The key is to reframe your thinking. Most home repairs aren’t true emergencies; they are predictable expenses that just happen on an irregular schedule. Your water heater will eventually fail. Your roof will eventually need replacing. The best way to handle these certainties is with a dedicated savings account: a home maintenance fund.

This isn’t the same as your general emergency fund, which is for life events like a job loss or medical issue. It’s also not a renovation fund for the kitchen remodel you’re dreaming about. A home maintenance fund is a specific financial tool designed to cover the cost of repairing and replacing the essential systems that keep your house running smoothly. Building one is one of the most powerful steps you can take to protect your investment and your peace of mind.

How Much Should You Save?

This is the most common question, and there isn’t a single perfect answer. The right amount depends on your home’s age, size, condition, and location. However, there are a few reliable methods you can use to create a solid savings target.

The 1% Rule

This is the most popular guideline for a reason: it’s simple. The rule suggests saving 1% of your home’s purchase price each year for maintenance.

- Example: If you bought your home for $400,000, your annual savings target would be $4,000, or about $333 per month.

This is a great starting point, but it doesn't account for the age of your home. A brand new home will likely need less than 1% in its first few years, while a 50-year-old home may require significantly more.

The Square Footage Rule

Another straightforward approach is to save $1 per square foot of your home’s living space annually.

- Example: For a 2,200-square-foot house, your annual savings target would be $2,200, or about $183 per month.

This method can be more accurate than the 1% rule in markets with very high or low property values, but it still doesn't factor in the age or condition of your home's major systems.

The Component-Based Method

This is the most accurate way to plan. It takes more effort up front, but it gives you a realistic target tailored specifically to your property. Here’s how it works:

- List Your Home's Major Systems: Write down the big-ticket items in your home, like the roof, HVAC system, water heater, and major appliances (refrigerator, oven, washer/dryer).

- Estimate Their Lifespan and Age: Research the typical lifespan for each item. The International Association of Certified Home Inspectors (InterNACHI) provides a useful life expectancy chart for this. Then, determine the current age of each component in your home.

- Calculate the Remaining Life: Subtract the current age from the expected lifespan.

- Estimate Replacement Cost: Research the average cost to replace each item in your area.

- Determine Your Annual Savings: Divide the replacement cost by the item’s remaining years of life. This gives you the annual amount you should be setting aside for that specific item.

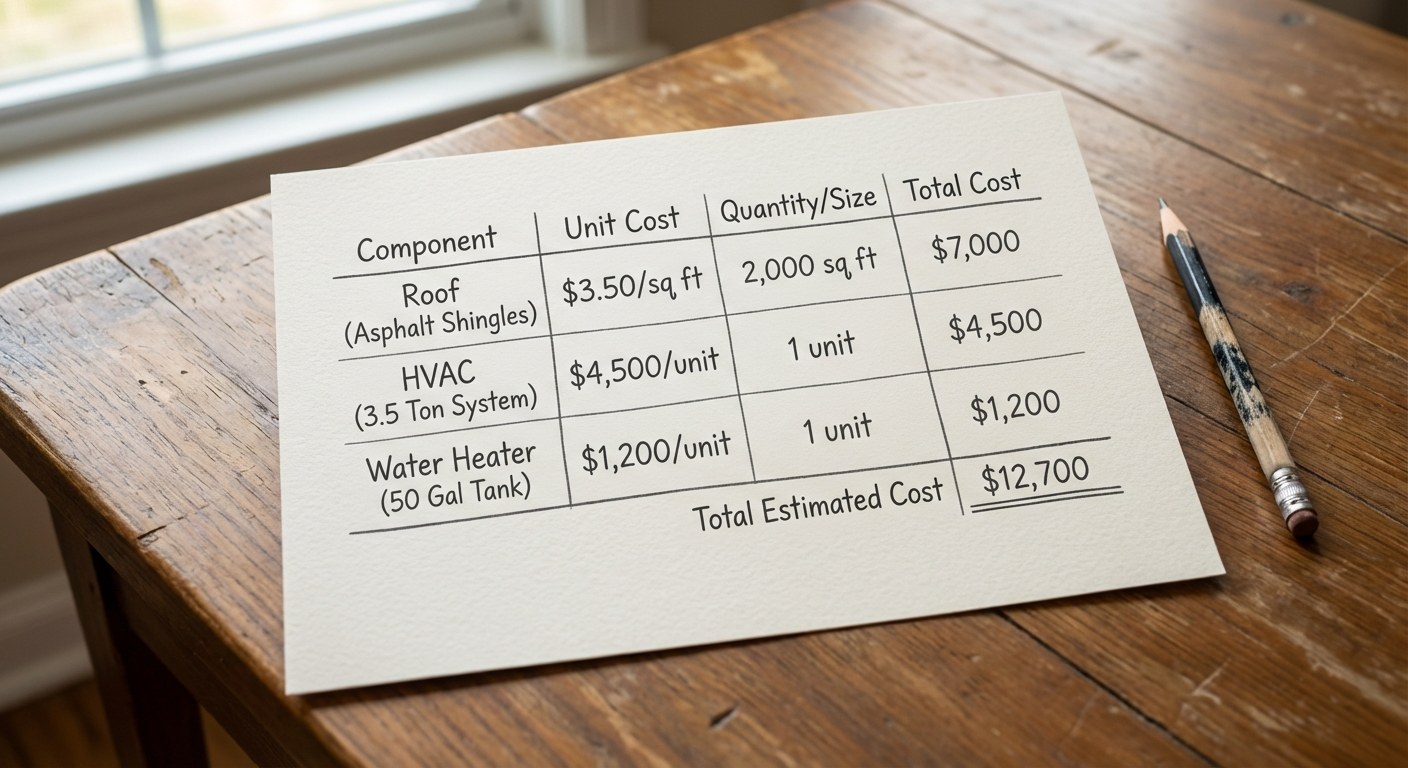

Image Alt: A table calculating the annual savings needed for a roof, HVAC, and water heater based on their replacement cost and remaining lifespan.

Image Alt: A table calculating the annual savings needed for a roof, HVAC, and water heater based on their replacement cost and remaining lifespan.

| Item | Est. Replacement Cost | Remaining Lifespan | Annual Savings |

| :--- | :--- | :--- | :--- |

| Roof | $12,000 | 10 years | $1,200 |

| HVAC System | $9,000 | 8 years | $1,125 |

| Water Heater | $1,800 | 5 years | $360 |

| Total | | | $2,685 |

This detailed approach can feel like a lot to manage, but using a home management app like Casa can make it simple to track the age and condition of your home’s systems, helping you build a more accurate financial plan.

Where to Keep Your Maintenance Fund

The goal is to keep this money safe, accessible, but separate from your daily spending.

The best place for your home maintenance fund is a high-yield savings account (HYSA). Here’s why:

- It’s separate: Keeping the money out of your primary checking account prevents you from accidentally spending it on groceries or other daily expenses.

- It’s liquid: You can access the money quickly when a repair is needed, without penalties.

- It earns interest: While not a wealth-building tool, an HYSA will earn a higher interest rate than a traditional savings or checking account, helping your money grow slightly over time.

Avoid the temptation to invest this fund in the stock market. While investing is essential for long-term goals, a home maintenance fund needs to be stable and available at a moment's notice, not subject to market fluctuations.

Getting Started and Staying Consistent

Knowing your target is one thing; reaching it is another. The key is to start now and be consistent.

- Start Small: If your annual goal feels overwhelming, don't let it stop you. Saving $50 a month is infinitely better than saving nothing. You can always increase the amount later.

- Automate Everything: This is the most effective way to save. Set up an automatic, recurring transfer from your checking account to your dedicated HYSA. Schedule it for the day after you get paid.

- Replenish After Use: When you have to pay for a major repair, the fund has done its job. Afterward, make a plan to build it back up to its target level.

Common Pitfalls to Avoid

As you build your fund, be mindful of these common mistakes.

- Mixing Funds: Avoid dipping into your maintenance fund for anything other than its intended purpose. It's for a broken dishwasher, not a new sofa.

- Ignoring Preventative Care: Don’t wait for things to break. Use the fund to pay for annual HVAC tune-ups or a professional gutter cleaning. A small expense now can often prevent a much larger one later.

- Setting It and Forgetting It: Revisit your savings goal every couple of years. Inflation, changes in your home’s condition, and rising labor costs can all affect your target number.

Your 3 Money Moves Checklist

Feeling ready to start? Here are three simple steps you can take today to build your financial buffer and reduce homeowner stress.

- [ ] 1. Calculate Your Target: Pick one of the methods above—the 1% rule is a great place to start—and determine your annual savings goal. Divide it by 12 to get a monthly target.

- [ ] 2. Open a Separate Account: Find a fee-free, high-yield savings account online. Give it a clear name, like "Home Maintenance Fund," to reinforce its purpose.

- [ ] 3. Automate Your Savings: Log into your primary bank account and set up a recurring monthly transfer to your new HYSA. Even a small amount builds momentum.

Building a home maintenance fund is a marathon, not a sprint. The goal isn’t just to save money; it’s to create a system that gives you confidence and control over your home and finances. By planning for these inevitable costs, you transform them from stressful emergencies into manageable events.

Taking charge of your homeownership journey is simpler when you have the right tools. The Casa app helps you track everything in your home, from appliance manuals to maintenance schedules, so you’re always prepared for what’s next. Download Casa today to start building a more organized, less stressful relationship with your home.

Related Reading